What is CS car finance?

Understanding Conditional Sale Car Finance

In the realm of car finance, CS car finance, also known as a conditional sale agreement or conditional sale finance, stands as a popular option, offering individuals a straightforward path to car ownership.

This guide will cover CS finance, explaining how it works and discussing its advantages and disadvantages. We will also compare CS finance with other options such as PCP and HP. Additionally, we will provide advice for individuals with poor credit and address common questions.

By the end, you'll have a clearer understanding of what CS finance is, empowering you to make informed decisions when considering your next car purchase.

What is CS Car Finance?

Conditional sale finance, also known as CS car finance or a conditional sale agreement, is a straightforward method of financing a vehicle purchase.

Unlike other finance options, with CS finance, you own the car outright once all payments, including any interest charges, have been made. Essentially, it's a loan secured against the vehicle, with the loan amount spread over an agreed-upon term, typically between 12 to 60 months.

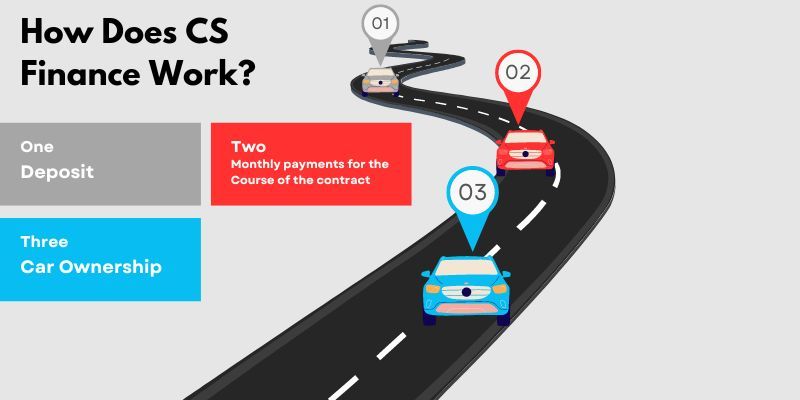

How Does CS Finance Work?

In a CS agreement, you pay a deposit upfront, typically around 10% of the car's value, although this can vary. The remaining balance, plus any interest accrued, is divided into fixed monthly payments over the agreed term. Once all payments are completed, the ownership of the vehicle is transferred to you.

Benefits of Conditional Sale Finance:

Ownership:

Unlike PCP where you have the option to return the car at the end of the term, CS guarantees ownership once all payments are made.

Flexible Deposit:

CS finance often allows for flexible deposit amounts, making it accessible to a wide range of buyers.

Fixed Monthly Payments:

With CS finance, monthly payments are fixed throughout the agreement, making budgeting easier.

No Mileage Restrictions:

Unlike PCP, there are typically no mileage restrictions with CS agreements, giving you more freedom to use the vehicle as you wish.

Drawbacks of Conditional Sale Finance:

Higher Monthly Payments:

Monthly payments on CS agreements are often higher compared to PCP, as you're paying off the entire value of the car to gain ownership at the end of the agreement.

Depreciation Risk:

As the owner of the vehicle from the start, you bear the risk of depreciation, which could impact the car's future value.

Ownership Obligations:

As the owner, you're responsible for maintenance and repair costs once the manufacturer's warranty expires.

Conditional Sale vs PCP:

PCP typically offers lower monthly payments, but at the end of the agreement, you have the option to return the car, purchase it outright (with a balloon payment), or part-exchange it for a new vehicle.

With CS finance, you will own the car at the end of the term without having to make a large final payment. However, you will have higher monthly payments.

Conditional Sale vs HP:

CS and HP are similar in that they both lead to ownership at the end of the agreement. However, HP often requires a larger deposit compared to CS, and monthly payments may be higher. Additionally, HP agreements often have an option to purchase fee at the end of the agreement.

CS Car Finance with Bad Credit:

Having a poor credit history can make obtaining traditional financing challenging, but CS finance can still be an option. Some lenders specialise in providing CS finance to individuals with bad credit, offering tailored solutions to suit their circumstances. At Cars 4 You, we understand the challenges of obtaining finance with bad credit and work with a range of lenders to find suitable options for our customers.

Conditional Sale Finance FAQs:

What if I can't afford the monthly payments?

It's essential to carefully consider your budget before committing to a CS agreement. If you find yourself unable to afford the payments, contact your lender immediately to discuss potential solutions.

What happens if I want to sell the car before the end of the agreement?

Selling the car before the end of the agreement can be complex, as you technically don't own the vehicle until all payments are made. However, you may be able to settle the finance early by paying off the remaining balance. However, some early repayment fees may apply depending on the finance lender.

What do I need to apply for CS finance?

Typically, you'll need to provide proof of identity, address, and income, along with details of the vehicle you wish to finance.

Is Conditional Sale Finance Right For Me?

Conditional sale car finance offers a straightforward path to vehicle ownership, with fixed monthly payments and no mileage restrictions.

While it may have higher monthly payments compared to other finance options, the assurance of ownership at the end of the term can be a significant advantage for many buyers.

If you need to know more about CS finance or you're considering CS finance and exploring your financing options, contact our finance team for personalised advice and assistance. We're here to help you find the right finance solution to suit your needs and budget.